Every year, more and more U.S. citizens renounce their citizenship, and green card holders give up their visa status—often without realizing that these actions can trigger the exit tax. The exit tax rules impose income tax on individuals who exit the U.S. tax system. A defining feature of these rules is the deemed sale of assets: individuals are treated as if they sold all their assets on the day before they give up U.S. citizenship or resident status. Net capital gain (after an exemption) from this deemed sale is taxed immediately.

Citizenship-Based Taxation

The United States follows a citizenship-based taxation system—meaning U.S. citizens and resident aliens are taxed on their worldwide income, no matter where they live. In contrast, nearly every other country (with rare exceptions like Eritrea) uses a residence-based model: you’re taxed only if you reside there. These citizenship-based principles are embedded in the Internal Revenue Code and are the reason why renouncing U.S. citizenship or residency is a taxable event, often triggering the exit tax.

The exit tax is the U.S. government’s way of settling your tax affairs before you permanently leave its jurisdiction. It addresses income that hasn’t yet been taxed—like capital gains on property—because such gains are typically taxed only upon disposal, which may not occur for years. Once you’re no longer under U.S. tax authority, the government can’t pursue future taxes—so the exit tax ensures it collects on unrealized gains accrued while you were a U.S. tax resident.

Who Should Worry About the Exit Tax?

The exit tax applies to two categories of people:

- U.S. citizens who terminate their citizenship; and

- Long-term residents — lawful permanent residents of the United States (holders of a “green card” visa) who terminate that status after holding it for many years.

If you do not fall into one of those two categories, you don’t need to worry about the exit tax rules. For instance, someone who has lived for decades in the United States under other visa types (student, H-1B, L-1A, etc.) will not be subject to the exit tax.

U.S. Citizens

Determining U.S. citizenship is usually straightforward—if you were born in the United States, you’re a citizen. It can be more complex for those born abroad to U.S. citizen parents, where eligibility depends on specific legal criteria. Naturalized citizens will typically have both documentation and clear memories of the process. In most cases, people know whether or not they are U.S. citizens. Dual citizenship doesn’t change this. Acquiring another citizenship will not terminate U.S. citizenship unless you successfully persuade the State Department that your acquisition of another nationality was intended to relinquish your U.S. citizenship.

Long-Term Residents

A resident is someone who holds lawful permanent resident (green card) status. A long-term resident is someone who has held that status for at least eight out of the last fifteen years. In making this “eight out of fifteen” calculation, special rules apply to disregard years in which the individual lived abroad and filed U.S. income tax returns as a nonresident under the terms of a tax treaty.

Example: For someone who became a lawful permanent resident in 2015 (and who has filed Form 1040 each year since), 2022 marks their eighth year of holding that status—they are now considered a long-term resident

What Actions Trigger the Exit Tax?

Giving up U.S. citizenship or long-term resident status.

Citizens Relinquish Citizenship: U.S. citizens can choose to give up citizenship by renunciation. The process is straightforward: file form DS-4079, answer some questions, pay a $2,350 fee, and make an oath in front of a U.S. Consular official to voluntarily renounce your U.S. citizenship. In a few instances, the government can take U.S. citizenship away, and when the process is complete, the State Department issues a Certificate of Loss of Nationality to confirm it.

Long-Term Residents Give Up Visa Status: Only green card holders who are long-term residents are affected by the exit tax rules. Once that status is reached, there are two ways a green card holder can trigger the exit tax:

- Voluntary abandonment: The green card holder files Form I-407 with USCIS, or the government may cancel the visa. This causes the individual to become an expatriate under exit tax rules.

- Treaty election: A green card holder elects to be treated as a nonresident under a tax treaty by filing Form 1040NR and attaching Form 8833. If this election is made after attaining long-term resident status, it will trigger expatriation

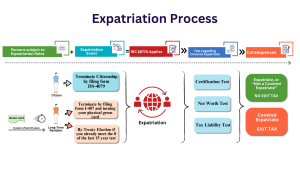

Are You a Covered Expatriate?

Once you determine that you’ve expatriated, the next step is figuring out if you are a covered expatriate—someone who may owe an actual tax, not just file paperwork. A covered expatriate meets any of the following:

- Tax Compliance Test: You fail to certify on Form 8854 that you complied with all U.S. tax obligations for the five years before expatriation.

- Net Worth Test: Your net worth is $2 million or more on the date of expatriation.

- Tax Liability Test: Your average annual net income tax liability for the prior five years exceeds a set threshold (e.g., $206,000 in 2025).

Covered expatriates are subject to the exit tax. Others are only required to file the necessary forms. Review the following diagram to better understand how the expatriation process works and whether the exit tax may apply to your situation.

What is an Exit Tax?

What is an Exit Tax?

The exit tax is a final tax calculation imposed on individuals who give up U.S. citizenship or long-term residency. It treats you as if you sold all your assets the day before leaving the U.S. tax system, taxing any unrealized capital gains as of that date. The amount you owe depends on the structure and value of your personal assets. Additionally, special rules apply to certain items such as IRAs, pensions, deferred compensation plans, and beneficial interests in trusts.

Planning Opportunities

With advance planning, you can reduce or avoid exit tax exposure. Some options include:

- Transfer assets to a U.S. citizen spouse to reduce net worth (the $2M threshold applies individually)

- Limit your average annual tax liability to stay under the income test

- Avoid meeting the 8-of-15 year rule for long-term residency

- Strategically shift ownership—e.g., transfer a home to your spouse and retain liquid assets

Conclusion

The exit tax rules are complex, and this article only scratches the surface. If you need help understanding the process or planning your next steps, don’t hesitate to reach out before taking action.